Ever since the price of Ethereum hit an all-time high above $2,000 last month, the number of addresses holding 10,000 or more ETH has barely changed, showing whales are holding onto their funds, despite the dip.

Data from on-chain analytics firm Santiment shows that wallets with over 10,000 ETH in them, worth over $18 million at press time, dropped by 0.9% over the last four months. The figure is compared to a 7.2% drop in the number of wallets holdings between 100 and 10,000 ETH.

The divergence could be associated with the nature of whale wallets on the blockchain. Some of these may be owned by organizations providing services in the space such as exchange, which need to keep the asset on hand. Institutional investors may also be considered.

Some of Ethereum’s circulating supply, it’s worth noting, has recently been locked in various decentralized finance (DeFi) projects and on the Ethereum beacon Chain. The Beacon Chain is a Proof-of-Stake (PoS) blockchain, and it signals the first step in the plan to change Ethereum’s consensus mechanism from Proof-of-Work (PoW) to Proof-of-Stake. It runs alongside the original Ethereum PoW chain, making sure that there is no break in the continuity of the chains.

According to its explorer, there are 3.5 million ETH staked on the Beacon Chain, worth over $6.3 billion. The locked funds are used by investors to become validators on the PoS network and earn a return on their ETH holdings while helping secure the network.

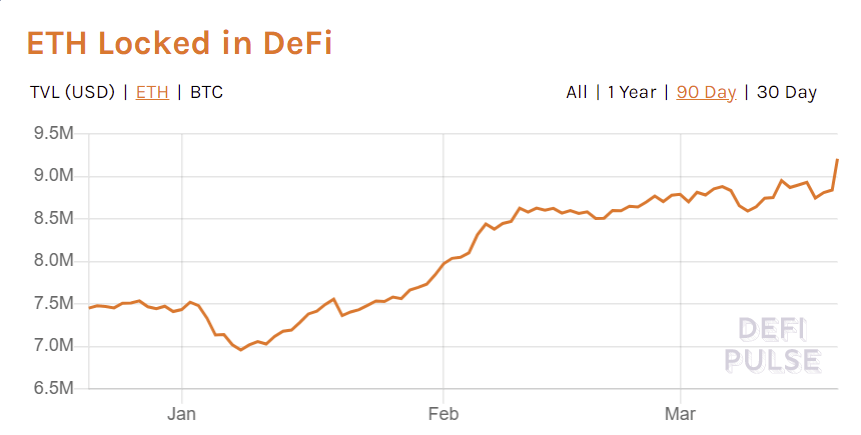

The amount of Ethereum locked in the decentralized finance (DeFi) space has also been growing steadily. Data from DeFiPulse shows there are now 9.2 million ETH locked in the space, which means that overall about 10% of Ethereum’s circulating supply is locked.

About 3 million ETH are locked on Maker, while SushiSwap, Compound, and Uniswap all have over 1 million ETH locked in them. According to CryptoCompare data, the price of ETH has been hovering around the $1,800 mark over the last few days.

Featured image via Pixabay.