The decision by Coinbase, announced earlier this week, to offer users the facility to store their private keys within a cloud based service has drawn the ire of many in the cryptocurrency community. However, it is an argument that appears to cut to the heart of the drive to fuel wider adoption of cryptocurrencies.

One of the noted maxims of many entrepreneurs when designing products is that it’s easier to leverage people’s behaviour than it is to change it. In the words of Keith Ferrazzi, author and Entrepreneur “Change is so damn tough, you can’t possibly imagine how tough it is and how incapable most of you are to change.”

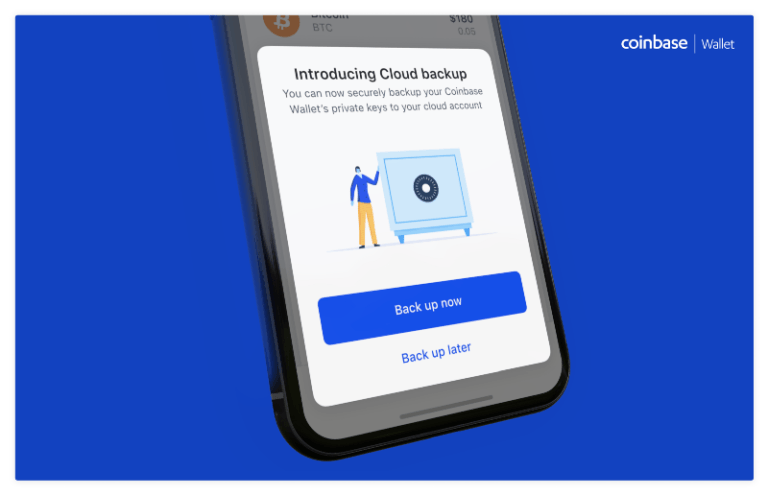

With this in mind, this recent announcement that cryptocurrency exchange Coinbase has made changes to its Coinbase Wallet app for iOS and Android allowing users to backup an encrypted copy of their private keys to the cloud (iCloud in the case of iOS users and Google Drive in the case of Android users) is not a strange one.

Yes, it may have irked much of the social media-commenting arm of the cryptocurrency industry; yes, it may fly in the face of much of the driving ethos of Bitcoin; yes, it may create a whole new data honeypot for hackers to target. However, in a world where the general public routinely hand over large trenches of sensitive data to companies in exchange for convenience, it makes a certain level of sense – although some consider it nonsensical for an industry that is built on the ideals of decentralization and self-sovereignty of money.

I for one applaud Coinbase's revolutionary new crowdfunded cloud storage honeypot. https://t.co/HX5UMWn2b9

— Peter Todd (@peterktodd) February 12, 2019

While the more security conscious among the cryptocurrency community may look at the idea of storing (even encrypted) private keys in the cloud and shake their heads in despair, the reality is that we live in a world where ‘trustless’ is a very niche area of interest.

We routinely leave sensitive financial information and access in the hands of large corporations like PayPal, Google, Apple and Amazon in exchange for the convenience of using their services – relying on backup questions to retrieve lost data (or similar storage facilities like Google Password or Last Pass). Ian Balina – a crypto personality – infamously got hacked after leaving his private keys in Evernote. Millions routinely leave their cryptocurrency funds in the hands of exchanges like Coinbase and Binance – and the limited uptake for decentralised options so far – DEXs account for only 0.19% of all trading volume according to CryptoCompare – appears to indicate that the market is more than happy with that arrangement.

It may not be the safest way of doing things, but it appears to be a level of risk and centralization that the majority consumers are happy with. We’ve all been raised in a culture where leaving our money in the ‘safe’ hands of banks has been the norm. Changing that culture is not going to be easy for those not ideologically or experientially inclined to do so. Many would look at this and see it as a relatively safe way to ensure they will never be permanently parted from access to their crypto wallets.

The Drive For Adoption

Currently, cryptocurrency appears to be at something of a crossroads where the early adopters and ideologues have taken it so far, but the kind of money that has been pumped into the sector can only be justified by wider adoption, indeed Coinbase’s lofty $8 billion valuation is not based on catering to a niche userbase that prides ideals over ease.. For that to happen, one suspects, some compromise to the behavioural economics of the real world would seem to be the order of the day. People generally trust that Google or Apple will keep their data safe, and they generally don’t want to be a single point of failure for a large part of their financial concern. They want an option; and this, perhaps, isn’t the worst of them.

As Daniel Larimer put it to me – and anyone else who would listen – earlier in the year: “when blockchain actually makes people’s lives easier and more secure, that’s when it’ll get widespread adoption.”

The idea that you are responsible for a twelve-word phrase, without which you could permanently lose your Bitcoin, is not making lives easier. Coinbase’s solution – however flawed – potentially does.

By way of contrast, on the very same day, Nick Szabo – one of the originators of the smart contract concept – describing the pursuit of adoption at the expense of trust-minimisation as a “penny-wise, and pound-foolish” approach to implementing the ethos of cryptocurrency.

“You want a really secure, trust-minimised, blockchain,” Szabo asserted, “We’re trying to build the Brinks trucks of the future, not the race cars.”

“So far,” Larimer added to his pitch, “the early adoption of Bitcoin and cryptocurrencies, is very philosophical. It’s inherently limited to people who actually believe in the cause. That’s true with all early adoption. It’s true with electric cars. It’s true with blockchain.”

From a certain point of view, holding the private keys to your money, and the inability of any bank or controlling authority to take that from you under any circumstances beyond outright coercion or threat, is empowering. However, to the vast majority of people, I suspect it is a chore that represents a single point of failure that they are reluctant to accept. Memories of the guy trawling a rubbish tip for his discarded bitcoin wallet, or of QuadrigaCX’s current missing-key woes, will live long in the memory. People value redundancy. They want an option.

According to the blog post by Coinbase Wallet Product Lead Siddharth Coelho-Prabhu, this new feature “provides a safeguard for users, helping them avoid losing their funds if they lose their device or misplace their private keys.”

It will utilise the same AES-256 encrypted data, accessible only via the Coinbase Wallet, that millions of us rely on every day to transfer sensitive data – and access our financial services. This is not new technology, it is merely technology that sits at an ideologically opposite point from that of the prevailing opinion of the cryptocurrency savvy Twitterati.

The bottom line, as always, is that it is a choice – at least for now. The cloud backup feature is currently opt-in, and other Wallets are available. Coinbase’s detractor have the right to voice their opinions too, and they may be proved to be right, but ultimately the market will decide on whether this is a good idea or not.

Coinbase, for its part, appears to be looking to address what I have come to know as the Star Trek/Star Wars/Doctor Who conundrum: how do you keep hardcore fans happy, while also attracting new people to the thing you’ve invested millions or billions into creating?

The answer, quite often, is that there’s actually no way to please the zealous fans of something, so it’s best not to try; indeed, one suspects, that such is Coinbase’s position in the market it is being damned for innovating, but would be damned for not.

The same people will likely criticise the company for one thing or another anyway.

At the @coinbase team meeting: “What's the dumbest thing we could come up with now that we've gone full shitcoin?”https://t.co/8JaLv8W7j4

— WhalePanda (@WhalePanda) February 12, 2019

In light of this, it’s better for Coinbase to ignore naysayers and follow its entrepreneurial tendency to provide something that works in a way that it believes most consumers will find solves a problem for them. That’s where their market, and their cache of new users will come from – not among the Twitter hoards that will naysay and gloat if it goes wrong.

Like all such situations, consumers will decide if it’s a level of risk they are comfortable with in exchange for convenience (pardon the pun).